Value Pick — July 5, 2026

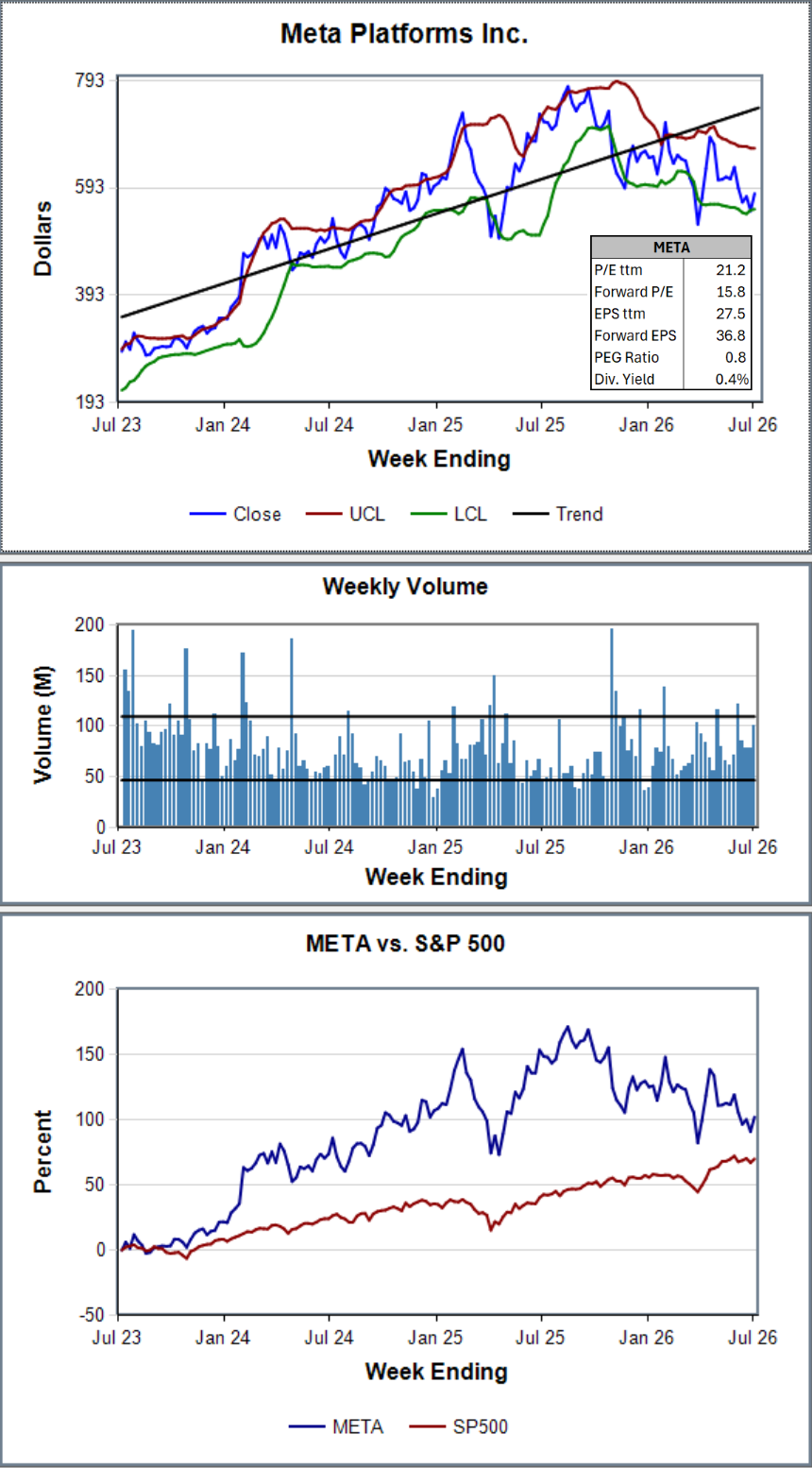

This week’s Value Pick is Meta Platforms (META). This is the second time we’ve picked Meta, the first time being on April 27, 2025. Since then Meta has gained 8.5% but is lagging the S&P 500 by 27.0%. On August 15, 2025 they reached an all-time high of $796.25 and is coming off a 26.8% dip since then. The fundamental metrics are excellent:

- P/E Ratio ttm: 21.2

- Price/Earnings/Growth (PEG) ratio: 0.8 (less than 1 is undervalued)

- EPS is expected to grow 33.8% over the next 12 months

With 58 Wall Street analysts rating META as Buy and only 6 as Hold with zero Sell ratings, a median 12-month price target of $825 representing a potential 41.5% upside from the current price of $582.90, it’s no wonder the analysts are bullish on META. We’re getting one of the sector’s highest-quality growth companies at a market-average multiple.

Market Summary

The S&P 500 gained 1.8% for the week, closing out the best quarter from major U.S. indexes since the pandemic in 2020.

- Monday kicked off the week with a Magnificent Seven rebound — after the prior week’s brutal tech selloff, battered mega-cap names bounced sharply as investors bought the dip, with the Nasdaq and S&P leading the recovery.

- Oil prices continued to slide, easing inflation fears — WTI crude was down nearly 20% over the prior two weeks as the Strait of Hormuz normalized following the Iran peace deal, reducing the energy-driven inflation pressure.

- Friday’s jobs report was the week’s decisive catalyst — only 57,000 jobs were created in June, roughly half the number expected — a “bad news is good news” report that pushed back expectations of a Fed rate hike.

How Our Past Picks Fared

Our past picks lost 1.9% to the S&P 500 during the week. They were essentially flat while the overall market gained 1.9%. This is despite a solid performance from three of our picks:

📈 CrowdStrike Holdings (CRWD) — UP ~10.7%

- CRWD’s gain was driven by a powerful combination of fundamentals, a historic analyst upgrade, and a stock split.

- CrowdStrike raised its full-year net new Annually Recurring Revenue (ARR) outlook by 520 basis points, with record Q1 net new ARR 32% year-over-year, ending ARR 24%+ growth, and free cash flow hitting an all-time record of $468.5 million at 34% of revenue.

- Three time recommended CrowdStrike popped 7% on June 29th, two trading days before its 4-for-1 stock split took effect on July 2, 2026 — with investors positioning ahead of the split date.

- As a result of the split, each of the original buy prices on the Scorecard has been divided by 4 to reflect the additional shares.

- The bigger fundamental catalyst was a massive Wells Fargo analyst upgrade: Wells Fargo analyst Michael Turrin raised his CRWD price target from $500 to $900 — an 80% jump — reframing how the desk is pricing the AI-security spending wave.

📈 CACI International (CACI) — UP ~10.8%

- CACI’s gain was a “value recognition” story — a deeply oversold defense IT contractor getting a second look after a series of punishing weeks.

- The macro backdrop helped significantly — the disappointing June jobs report (only 57,000 new jobs) pushed back Fed rate hike expectations, which benefits defense IT contractors through lower discount rates applied to their long-duration government contract revenue streams.

- The stock had become deeply oversold: Simply Wall St’s DCF model estimated CACI’s intrinsic value at approximately $882 per share versus a recent price around $503 — implying a 42.9% undervaluation — with the stock scoring 5 out of 6 on their quality checklist despite the selloff.

- The underlying business metrics remained strong: Q3 FY2026 EPS beat the forecast by 4.3%, revenue was up 8.5% year-over-year, and the company raised full-year revenue guidance.

- A new senior appointment reinforced confidence in execution: CACI appointed returning executive Tom Kirkland as EVP of Electronic Warfare — a signal that the company is building out its technology differentiation in one of the Pentagon’s highest-priority spending areas. Kirkland previously served as VP of Business Development at CACI from 2016–2020, then rose to President of the Targeting and Sensor Systems Sector at L3Harris Technologies before returning.

📈 Zscaler (ZS) — UP ~11.4%

- The “SaaSpocalypse” fear — that AI would cannibalize enterprise SaaS — received a significant counterpoint: Guggenheim’s John DiFucci upgraded both Salesforce and ServiceNow to Buy, arguing the AI-disruption fear had pushed valuations too low.

- The scale of the opportunity was notable: Zscaler was trading 59.1% below its 52-week high and down 37.6% year-to-date — a stock this far below its highs doesn’t need a lot of fresh buying to generate an outsized percentage move.

- The week’s 11.4% gain, while substantial, should be viewed in context — ZS remains one of the year’s worst-performing large-cap software names, and the analyst consensus price target of $213.97 is still roughly 40%+ above where the stock is trading even after the bounce.