Value Pick – May 17, 2026

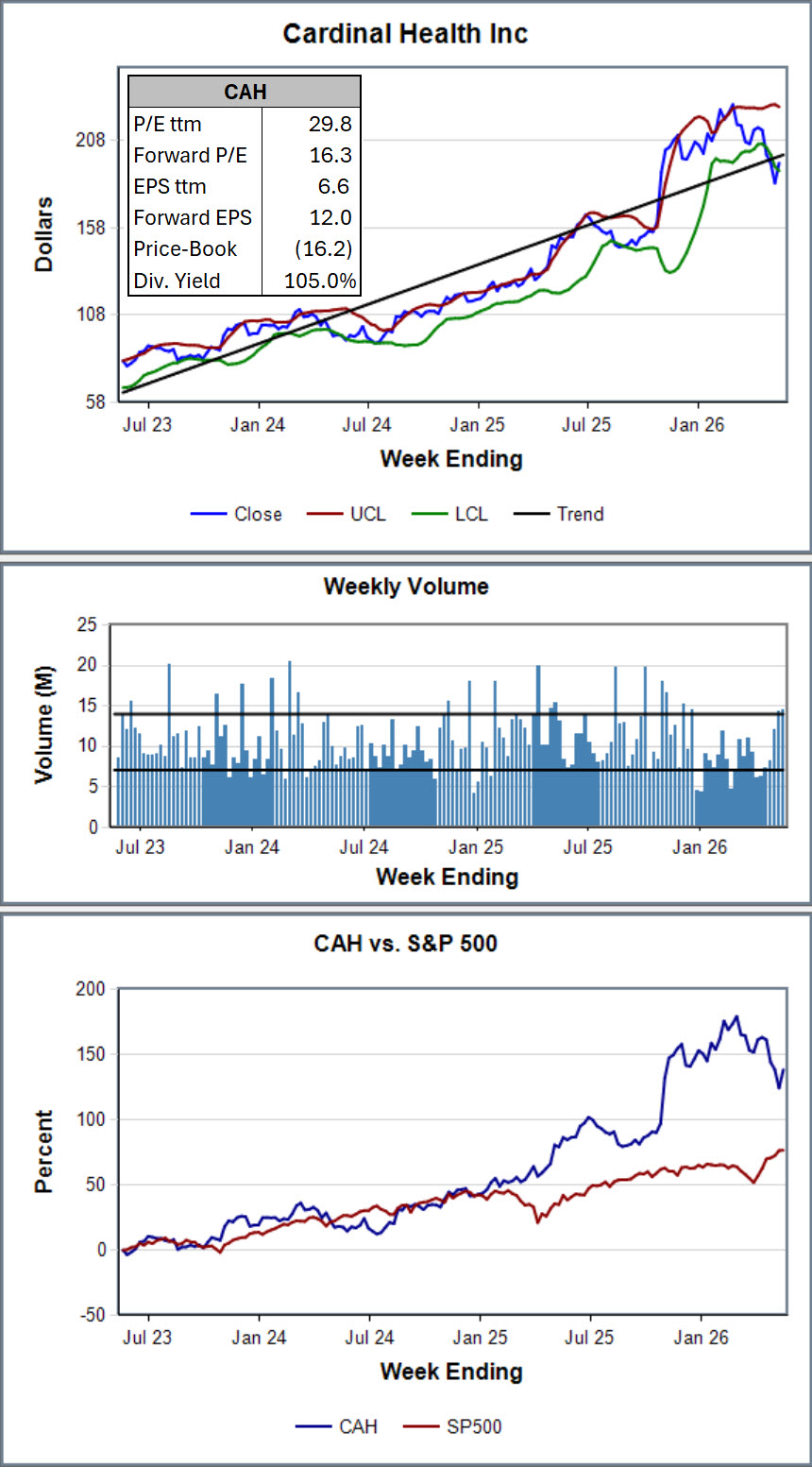

This week’s Value Pick of the Week, after a seven week drought, is Cardinal Health (CAH). The healthcare sector is trailing the S&P 500 by 5.9% this year and past pick UnitedHealth (UNH) is down 43% over the past 12 months. Recently there have been signs that the health services sector is turning around, and Cardinal has been outperforming the sector and the S&P 500 for the past five years. This past week: UNH +3.7%; Elevance Health (ELV) +3.9%; CVS Health (CVS) +5.9%, with CVS gaining 38.0% since March 26th.

- Earnings momentum is strong — FY2026 EPS guidance raised to a level that implies 30% YoY growth

- Valuation is reasonable — Forward P/E of 16.3 for a company compounding earnings at 30%+ annually is attractive

- Wall Street agrees — 12-analyst Buy consensus with an average price target of $241 (+23.5%)

- Shareholder-friendly — recently raised its quarterly dividend; consistent buyback program

- Entry point looks favorable — stock is down 9.4% YTD and pulled back further after a minor Q3 revenue miss, despite raising full-year guidance

Market Summary

This past week was volatile, but in the end the S&P 500 was up 0.1%. A gain is a gain.

- Record High Close — the S&P 500 hit a new record close of 7,501.24 on Thursday, closing above the 7,500 mark for the first time in its history

- Friday Tailspin — the S&P 500 fell 1.2% on Friday, wiping out what was set to be a very good week

- The CPI report on Tuesday was hotter than expected but obscured by President Trump’s trip to China

- Treasury yields reaching the highest level in a year combined with the CPI report and the end of Jerome “Too Late” Powell’s regime made future rate hikes a possibility

- President Trump’s meeting with China’s Xi ended on Thursday with the topics of tariffs, semiconductors, and export controls still on the table, and tech sold off sharply on Friday as a result

How Our Past Picks Fared

Our past picks gained 1.5% versus the S&P 500.

Notable Movers (±10%)

📉 Napco Security Technologies (NSSC) — DOWN 11.3%

- Napco continued to be punished for its miss last week. This kind of two-wave selloff is a recognizable pattern with small-cap stocks:

- Wave 1 — the immediate algorithmic and institutional reaction on earnings day

- Wave 2 — the slower bleed as retail investors catch up, analysts revise estimates, and funds that missed the initial move trim or exit positions

📈 Ford Motor Company (F) — UP ~10.1%

- Reported Q1 2026 adjusted EPS crushed expectations by 247.4% and revenue came in 11.5% higher — a massive beat on both lines

- Management raised full-year adjusted EBIT guidance by 23.5%

- Morgan Stanley issued a bullish report on Ford’s new Energy business, contributing to a 13% single-day surge on May 13th — Ford’s largest single-day gain since March 2020

- Ford’s Energy initiative, a battery collaboration with Contemporary Amperex Technology (CATL), and a consumer pricing campaign reinforced the narrative that Ford’s turnaround is broadening beyond its core auto business

📈 CrowdStrike (CRWD) — UP 12.6%

- Gain was not earnings-driven — CrowdStrike had not yet reported; this was a momentum and sentiment story

- Primary catalyst was peer Fortinet (FTNT) delivering blowout quarterly earnings, triggering a broad cybersecurity sector rally as investors rotated into the space ahead of upcoming earnings reports

- CrowdStrike released a report showing cyberattacks on financial institutions surged 43% globally, reinforcing the structural demand narrative

- By Friday May 15th, CRWD had posted its seventh consecutive day of gains, closing at $594.08 and up 42% over the prior month