Comparison of QQQ, QTUM, and WQTM

Exchange Traded Funds (ETFs) are a great way to instantly diversify a portfolio and they’re a great way to enter the market when you first begin investing. When you buy a share in an ETF you’re buying a basket of companies. The most popular type are the S&P 500 Index ETFs — there are many of them (SPY, IVV, VOO, etc.) and they’re all made up of the 500 largest companies traded on US exchanges, so when you buy a share of SPY you’re getting a small part of each of those 500 companies.

There are numerous different types of ETFs, with some tracking other indexes like the Russell 2000 or the Dow Jones Industrial Average, and others tracking various sectors of the economy like Manufacturing or Healthcare. Recently, Shane Hughes with Strategic Partners — a friend and fellow investor who knows about my keen interest in anything related to quantum computing — brought the Wisdom Tree Quantum Computing Fund (WQTM) to my attention. It seemed like a good time to compare WQTM to two other ETFs that have been discussed in the Value Pick of the Week: the Invesco QQQ Trust (QQQ) and the Defiance Quantum ETF (QTUM).

Overview

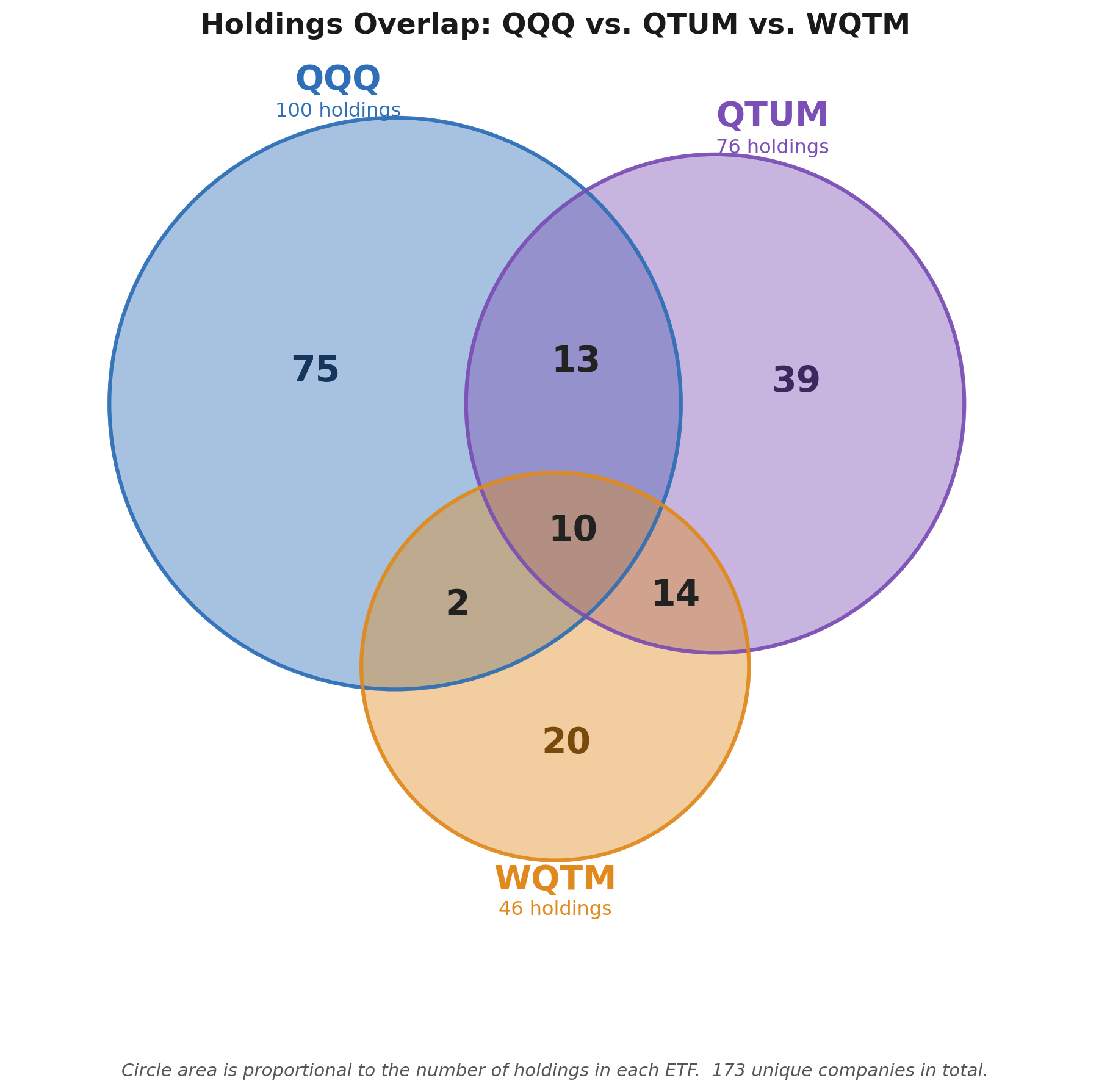

The three ETFs have a combined 170 unique companies:

- QQQ is the most diverse of the three, with 100 companies

- QTUM focuses on 85 quantum and quantum-adjacent companies

- WQTM is close to a pure quantum play with 46 components

QQQ vs. QTUM

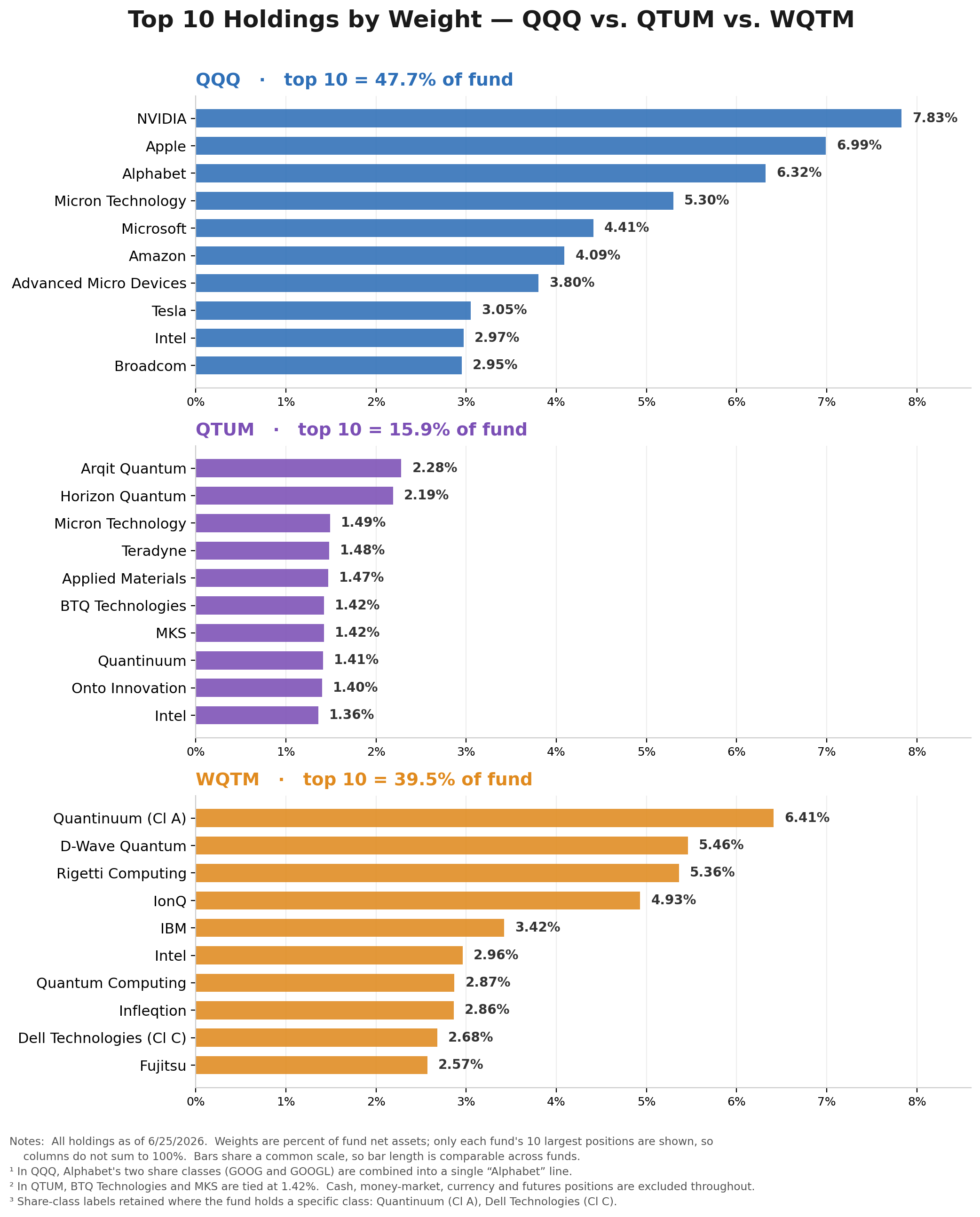

QQQ is nearly a subset of the S&P 500, with 86 companies in both QQQ and S&P 500 Index funds like SPY, VOO, and IVV. If you have S&P 500 ETFs in your portfolio, buying QQQ will add to your exposure of the Magnificent 7 — Nvidia (NVDA), Apple (AAPL), Alphabet (GOOG), Microsoft (MSFT), Amazon (AMZN), Tesla (TSLA), and Meta Platforms (META) — with roughly 35% of QQQ’s value coming from those seven companies.

Fourteen of QQQ’s 100 holdings sit outside the S&P 500, and nine of them are excluded for a single structural reason: they aren’t headquartered in the United States. The S&P 500 admits only U.S.-domiciled companies, while the Nasdaq-100 behind QQQ has no such rule and asks only for a Nasdaq listing. That gap captures some genuinely large, well-known names — the Dutch chip-equipment maker ASML Holding (ASML), Britain’s chip-design firm Arm Holdings (ARM), e-commerce players Shopify (SHOP) in Canada, MercadoLibre (MELI) in Latin America, and China’s PDD Holdings (PDD), parent of Pinduoduo and Temu; the Netherlands-based AI-cloud company Nebius Group (NBIS), formerly Yandex; infrastructure operator Ferrovial (FER); bottler Coca-Cola Europacific Partners (CCEP); and Canada’s Thomson Reuters (TRI). Several of these are easily large enough for the S&P 500 by market value — they’re kept out purely by geography.

The remaining five are American companies that are eligible but simply haven’t been selected, a reminder that S&P 500 membership is decided by a committee against criteria like sustained profitability, liquidity, and float rather than size alone. Three are recent arrivals to the public markets that the index typically lets season first: CoreWeave (CRWV), which IPO’d in 2025, plus Astera Labs (ALAB) and Rocket Lab (RKLB). Alnylam Pharmaceuticals (ALNY) is a sizable biotech that hasn’t yet been tapped. The most distinctive case is Strategy (MSTR), the Bitcoin-accumulating company formerly known as MicroStrategy, which has repeatedly been passed over in part because its earnings profile and crypto-driven balance sheet sit awkwardly against the index’s profitability test. The flip side of that test is worth noting: Marvell Technology (MRVL) was in exactly this “QQQ but not S&P 500” bucket until it finally cleared the profitability bar and joined the index on June 22, 2026.

QTUM vs. WQTM

The similarity is a shared core. The two funds hold 33 of the same companies, and that core is essentially the entire quantum theme: the pure-play quantum names (Quantinuum, D-Wave, Rigetti, IonQ, Quantum Computing, Infleqtion, Xanadu, Arqit, BTQ, Quantum Emotion), the big-tech quantum programs (IBM, Microsoft, Amazon, Alphabet, Nvidia, Intel, AMD), the semiconductor-equipment and Electronic Design Automation (EDA) backbone (Applied Materials, Lam Research, ASML, TSMC, Synopsys, Cadence, Coherent, Infineon, STMicro, NXP), and a cluster of Japanese tech (Fujitsu, Hitachi, NEC, NTT). Because that overlap accounts for 81% of WQTM but only 39% of QTUM, WQTM is close to being a concentrated subset of QTUM rather than a genuinely different portfolio.

The first difference is breadth. QTUM nearly doubles the holding count, and its 52 unique names push it well beyond “quantum” into the broader advanced-computing supply chain: chip designers and equipment (Marvell, Qualcomm, Broadcom, ADI, Microchip, ARM, Tokyo Electron, KLA, Onto, MKS, Teradyne), AI/data-infrastructure software (CoreWeave, Cloudflare, Snowflake, MongoDB, Palantir, Baidu, Alibaba), and even aerospace/defense and industrials (RTX, Lockheed, Northrop, Airbus, Honeywell, ABB). QTUM is really a “quantum + AI + advanced semiconductors” basket. WQTM’s 13 unique names go in a narrower direction — a telecom and quantum-networking tilt (Deutsche Telekom, SK Telecom, SES satellites, Ciena) plus quantum-security small caps (SEALSQ, Creotech) and a few foundry/test names (GlobalFoundries, FormFactor, SkyWater, Keysight, Corning).

The bigger difference is how they weight the shared names — and it’s the whole story for an investor. QTUM’s modified equal-weight scheme flattens everything to roughly 1%, so its largest holding is just 2.28% and the pure-play quantum stocks sit mid-pack alongside Oracle and Texas Instruments. WQTM deliberately concentrates in the pure-plays: Quantinuum, D-Wave, Rigetti, and IonQ are its top four at roughly 5–6% each, about 22% of the fund combined. Those same four names total only about 4.5% of QTUM — so WQTM gives roughly five times the direct pure-play quantum exposure. The mega-caps that anchor QQQ (Nvidia, Microsoft, Amazon, Alphabet) are held at roughly 1% in QTUM and roughly 2.5% in WQTM, deliberately sized down in both.

QTUM is the diversified, lower-volatility way to own the quantum supply chain, where pure-play quantum is a minority sleeve inside a broad AI portfolio; WQTM is a concentrated, higher-beta bet (higher risk and volatility) on the pure-play quantum-computing companies themselves, with a side of quantum networking and security. Same theme, very different risk profile.

Relative Performance

We repeatedly hear the phrase “the tech-heavy NASDAQ,” but that’s somewhat of a misnomer — 41% of the NASDAQ listings aren’t in the information technology sector, including companies like Costco (COST), PepsiCo (PEP), and Old Dominion Freight Lines (ODFL). On the other hand, QTUM is really a broad “next-generation computing” basket. A lot of the fund is effectively a bet on the semiconductor and AI infrastructure ecosystem that may benefit from quantum computing, rather than a pure bet on companies building quantum computers. QTUM isn’t a “quantum pure-play” technically, but its near equal-weighting prevents mega-cap companies like IBM, Microsoft, and Intel from overwhelming the small-cap companies that are focused completely on quantum computing.

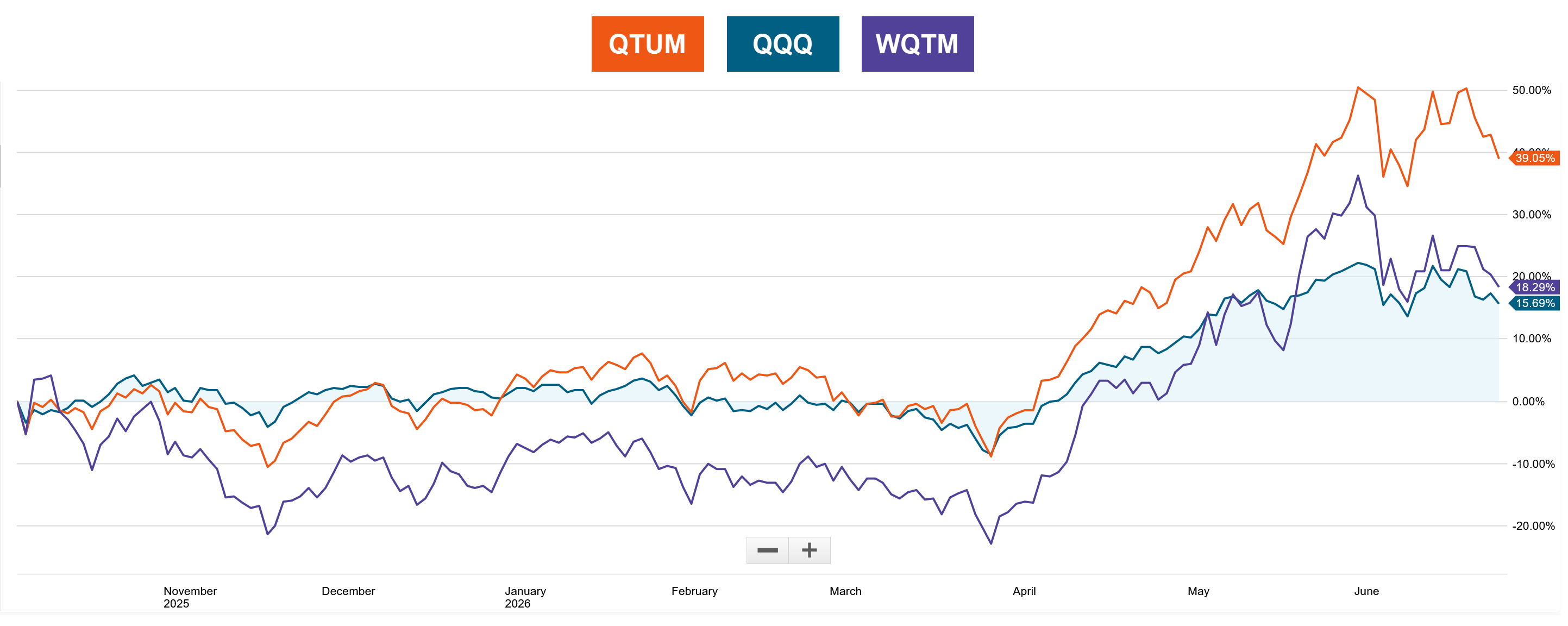

Looking at the past five years, QTUM is the clear winner over QQQ — 213% to 100%. There’s no valid five-year comparison with WQTM; it’s a newcomer that started trading on October 9, 2025.

Comparing the same three ETFs since the inception of WQTM, the picture changes somewhat. QTUM is still the winner, surpassing both QQQ and WQTM by significant margins, but over the past nine months WQTM has a slight edge of +2.6% over QQQ.

Conclusion

Given the certainty of quantum computing in the foreseeable future, both QTUM and WQTM have strong growth potential. Given the nature of business and the accelerating number of mergers and acquisitions, it wouldn’t be a surprise to see one or more of the mega-caps in both ETFs — Intel, Nvidia, Microsoft — acquiring some of the small-cap companies that are exclusive to WQTM. Considering all of this, and the fact that QTUM shares 33 of 46 companies with WQTM, QTUM is the clear choice for a quantum computing investment. In fact, over the past three years it has crushed the S&P 500 — 208.2% to 68.1%.